- 07/06/2022

- CN30

Reinventing Steel for a Sustainable Future

Sandip Biswas is Group Chief Investment Officer at GFG Alliance and Interim CEO, Primary Steel & Mining Europe & Australia at LIBERTY Steel. In his keynote speech at Fastmarkets Steel Success Strategies 2022, Sandip spoke of the long-term trends affecting steel and LIBERTY’s approach to the GREENSTEEL transition

At a glance

9 min read

- Steel demand could almost double by 2050 and must be met with sustainable solutions

- Successful steel companies of the future will be those that can transform to GREENSTEEL technologies quickly

- A supportive policy environment, renewable energy supply, increased demand, investment, and human resource are crucial for the GREENSTEEL transition

LIBERTY, just like all steel producers, has a large task in front of us to decarbonise our operations – but we have a positive view on the long-term prospects of our industry.

We expect the population to continue to grow, particularly in the developing world. India’s population, for example, is expected to reach 2bn within a generation. This will continue to drive demand for steel as a growing middle class seek out cars, homes and consumer goods.

It is anticipated therefore that steel demand could almost double by 2050. But as we all know – that demand must be met sustainably to avoid the worst effects of climate change.

We believe the successful steel companies of the future will be those that can transform to GREENSTEEL technologies quickly.

This transition will have major implications for primary steel production, which we believe will gravitate to the places that can provide cheap, abundant and secure renewable energy essential to the GREENSTEEL transformation.

So why do we see the need to act quickly and set ourselves the significant challenge to decarbonise well before 2050?

The steel industry is facing what we describe as a trilemma

Steel accounts for around 8-9% of global CO2 emissions, 10% if you include aluminium. Yet, as I said earlier, demand is going up.

And we are now seeing increasing regulatory pressure for steel companies to decarbonise. Europe has the lead but now the US, Australia and even China are catching up.

So, if we’re serious about climate change, and we want to continue to operate and capture the value in that growth, we need to change. And we need to change quickly.

According to the Net Zero Steel Initiative early progress on steel decarbonisation could unlock 1.3Gt of CO2 emissions reductions in 2030. That’s the approximate CO2 saving of taking every vehicle off the road in the US for two and a half years.

It’s this early action that will help keep the target of limiting global warming to 1.5 degrees alive.

But as well as helping the climate, decarbonisation can also be a massive opportunity for steel consumption.

According to a McKinsey Report steel is the most critical material for the transition to a low carbon economy, from electric vehicles to nuclear power.

So how do we plan to achieve the transition to GREENSTEEL?

We see two major pathways depending on the local market dynamics.

- Combine steel scrap recycling with renewable power

In mature markets such as the UK and US, it makes sense to utilise the growing arisings of scrap available locally. - Introduce breakthrough technology to address emissions from primary steel making

Not every country is currently optimising the potential. For example, in the UK there is enough scrap steel generated each year to satisfy the demand for new steel. Yet the UK currently exports 80% of its scrap without any added value, and the majority of UK steel production relies on imported raw materials which are increasingly risky. Our strategy in these markets is to optimise the available scrap and increasingly power our industrial processes with renewable energy.In this respect the US is already ahead with 70% of its production coming from EAFs and a domestic scrap utilization of approximately 85%.Of course, with the growing demand for steel, there is not enough scrap to satisfy global demand.So we need primary production, but primary production needs to decarbonise, which is where breakthrough technology needs to be proved and applied.

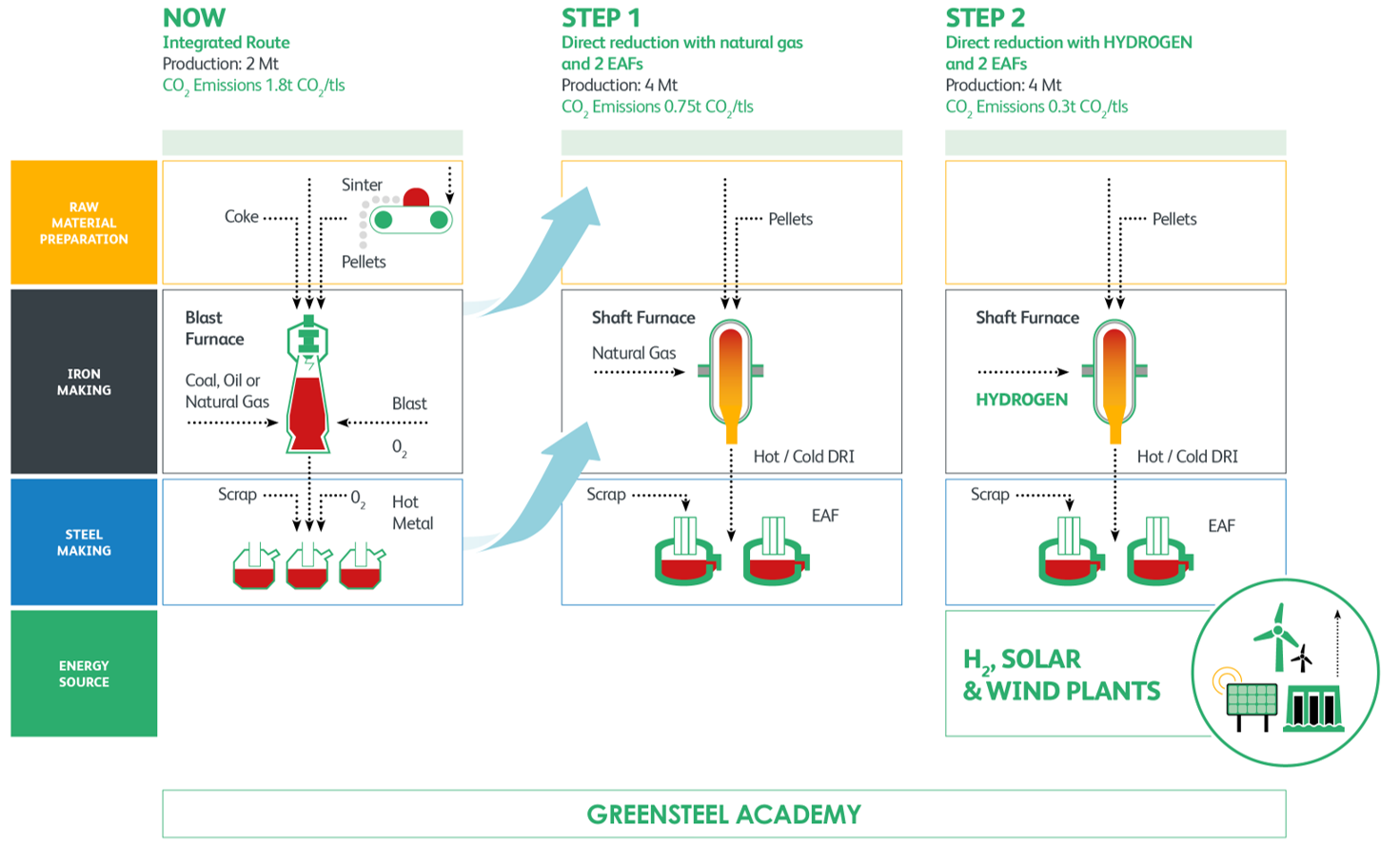

Here’s how we see the GREENSTEEL transition for primary production

Right now, we have conventional primary steel production – coal combined with iron ore with high CO2 emissions.

Step One: The transition to DRI furnaces using natural gas as the reducing agent for iron ore. Process DRI in EAFs with scrap. This reduces CO2 emissions by nearly 60%.

Step Two: As green hydrogen becomes viable, switch gas for hydrogen as the reduction agent for iron ore. Maximize renewable energy usage.

Through this transition we can take emissions from around 1.8 to 0.3 tonnes of CO2 per tonne of steel.

Our plant in Whyalla, South Australia, is a great example of our strategy in action

Whyalla enjoys ideal conditions for green steel production, including vast magnetite iron ore reserves, abundant solar and onshore wind energy, a deep-sea port and a skilled workforce.

South Australia has also just elected a very forward-thinking Premier, Peter Malinauskas, who has committed to building a 250Mw hydrogen production plant in Whyalla by 2025 which will massively support our plans for hydrogen steel making at our steel plant.

And we’re putting in place the other building blocks for that to happen with our magnetite expansion project, which is important because high-quality processed magnetite ore is essential to the DRI process for making GREENSTEEL.

We have big plans which are taking shape today. In April we announced the first phase of our magnetite expansion project which will increase production to 2.5mtpa. The second phase is set to lift production to 5mtpa to ensure there is enough high-quality iron ore for DRI production in Whyalla.

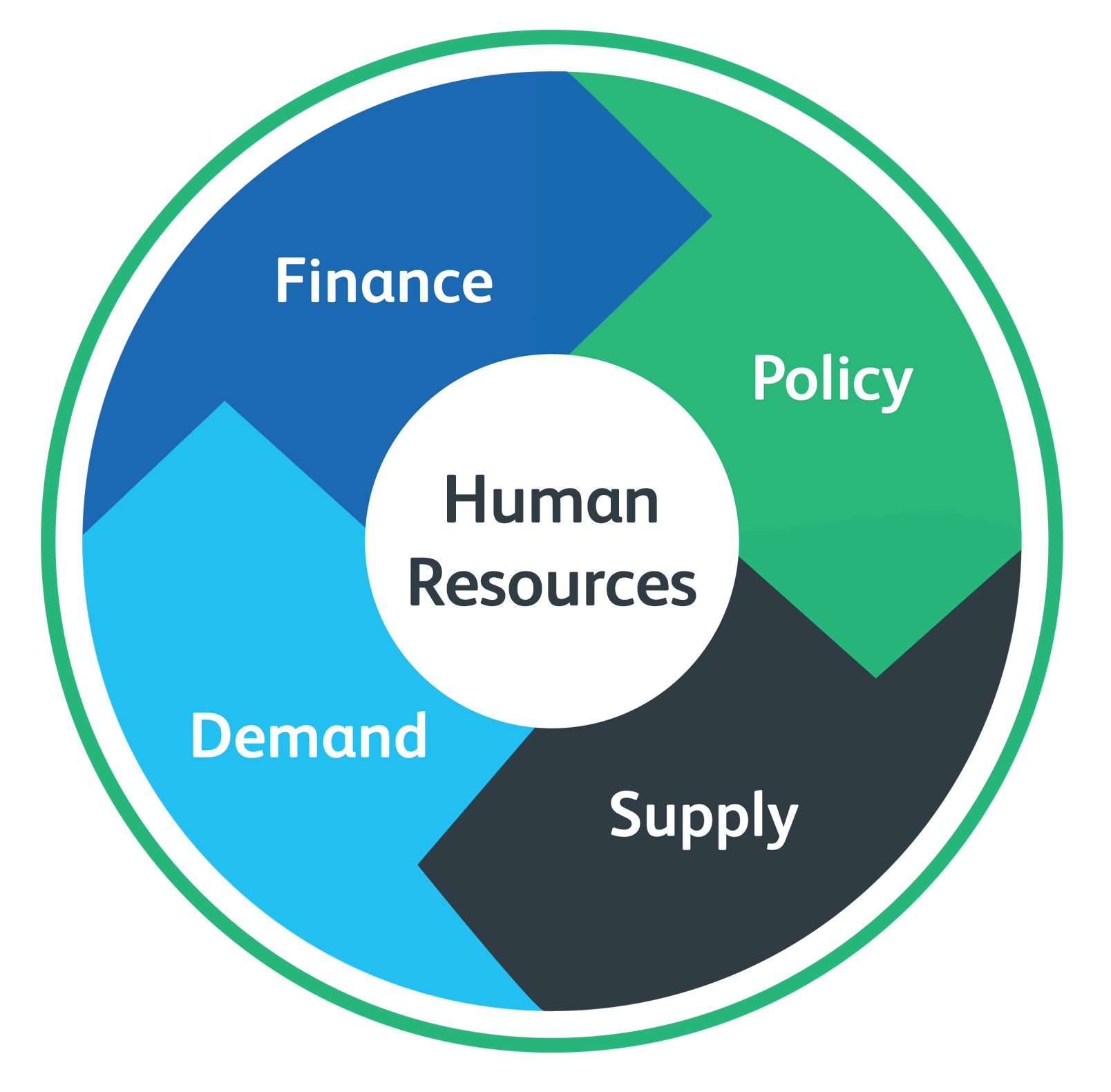

Here are the five key enabling factors that are vital to the transition to GREENSTEEL

|

This needs to balance incentives with regulation. Implement policy that is too strict too quickly, adding costs or reducing competitiveness, you compromise industry’s ability to invest in the transition, but if you do nothing the industry won’t move quickly enough. Policy incentives are therefore required to support industry and ensure that companies which implement low carbon technologies are rewarded.

Abundant, secure and cheap renewable energy is required. Scrap will increasing become a precious commodity will high-quality iron ore for Direct Reduced iron (DRI) and Hot Briquetted Iron (HBI) production will be key. In that respect we believe primary production will gravitate towards geographies best placed to supply these inputs competitively.

Demand for green steel is still low across the steel consuming sectors but growing particularly in automotive and in public sector procurement criteria. We believe demand will increase quickly as green steel become available and that will attract a premium.

The transition to low carbon technologies will be expensive. According to the Net Zero Steel Initiative the sector will need to invest more than $36bn each year to meet the high demand of the future and fund the transition to low carbon technologies. It is clear that steel companies on their own cannot make all this investment and will require support from Governments (policy and investment) and the global financial industry.

The most important resource of all. The demographics of the global steel industry, particularly in the west, are against us with an ageing workforce and fewer and fewer young people seeing the steel industry as a sector of choice. At LIBERTY over 20% of our workforce is over 55. But we are taking action through the development of our GREENSTEEL Academy, which aims to upskill the plant’s current workforce and encourage new people into the industry. The GFG Foundation is also seeking to inspire future generations into our industry through education and work placements, with programmes already set up in Australia, Romania and the UK, and plans to into the Czech Republic.

|

Sandip Biswas gave this keynote speech at Fastmarkets Steel Success Strategies Conference 2022 in Miami, USA

Latest News

View All Media Releases

Media Releases

Tees Mayor visit highlights rich energy pipeline potential at LIBERTY Pipes Hartlepool

Tees Valley Mayor Ben Houchen has highlighted the rich potential for LIBERTY Steel’s Hartlepool operations to lead the UK energy...

View Media Releases

Media Releases

LIBERTY appoints Thomas Gangl as CEO of its European business

LIBERTY Steel Group (“LIBERTY”) has appointed international sustainability leader Thomas Gangl as the Chief Executive Officer of its European business,...

View Media Releases

Media Releases

LIBERTY announces UK strategic steel plan after signing new creditor framework agreement

LIBERTY today announces the strategic plan for its UK steel assets after signing a new framework agreement (“the framework”) with its major creditors. The new framework comes after...

View Media Releases

Media Releases

LIBERTY Steel selected for major UK carbon capture pipeline contract

LIBERTY Steel today announces that its Hartlepool pipes division has been selected for a major contract to supply pipelines to...

View